Plan With a Total Balance Sheet, Including Invisible Assets and Liabilities

A financial plan should be a thoughtful alignment of your income, expenses, saving, and asset allocation that makes it more likely you’ll achieve what matters most to you. Your estate plan is financial plan’s autopilot, ensuring that your capabilities carry out your goals, even if you’re not around to supervise things yourself.

Using the Quadrant-based life cycle planning model, your balance sheet is one of your key Facts, because it presents your capabilities and your obligations on a single page.

A conventional balance sheet (one that shows your “visible” assets, liabilities, and net worth) shows the capabilities and obligations you have presently.

In theory.

In reality, your conventional balance sheet is likely leaving out some (or even most of) the really important stuff.

Good stuff such as your stream of future earnings or your plans to put your child through medical school. Bad stuff, like your spouse’s compulsive shopping. Or stuff that might be good, or bad, depending on your perspective, like your hobby of collecting boats, cars, or watches.

To show all of your capabilities and obligations, you need to include these “invisible” assets and liabilities, to produce a Total Balance Sheet.

A thoughtful consideration of your Total Balance Sheet should be one of key engines for your integrated financial and estate plan.

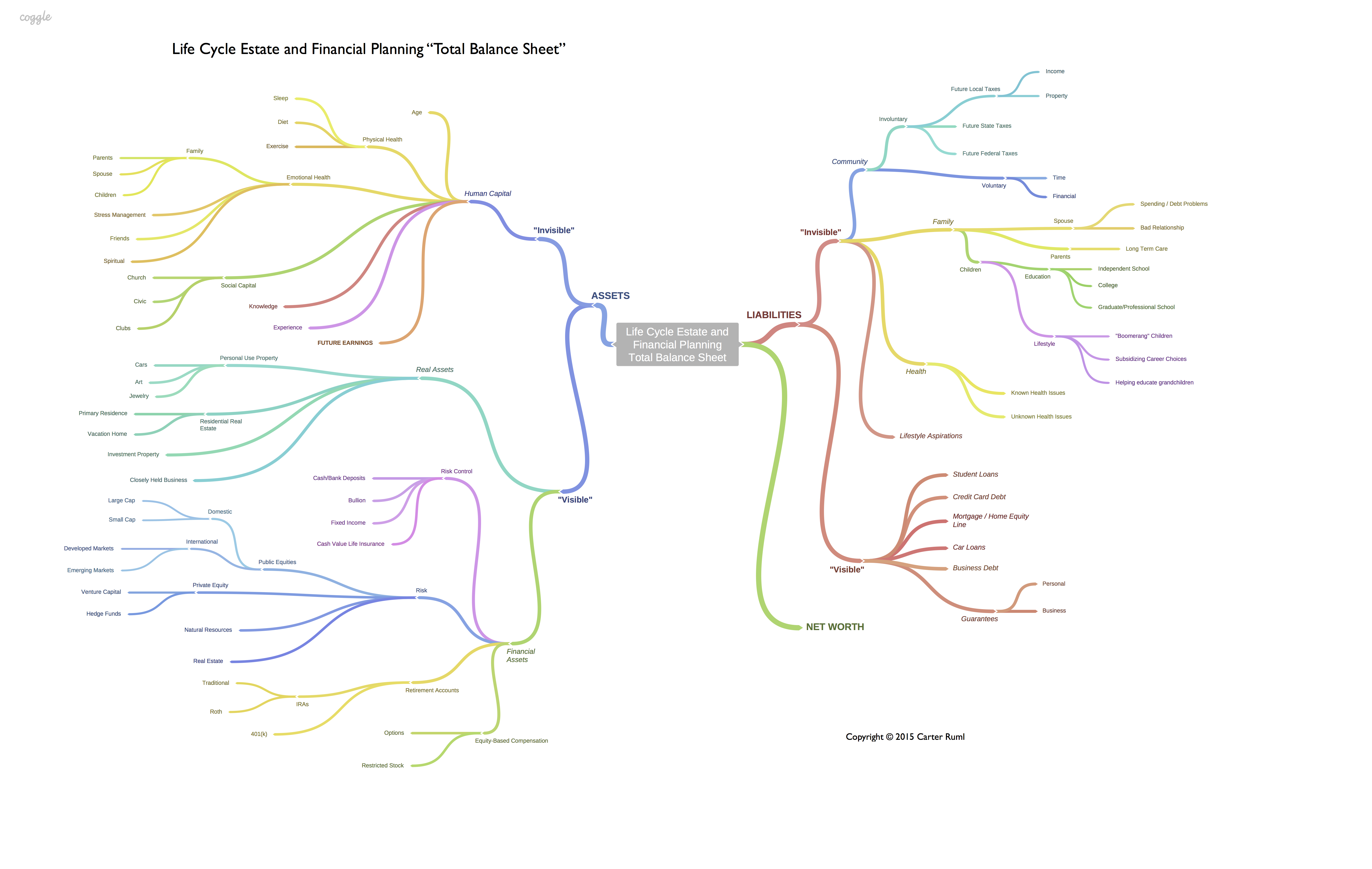

The Total Balance Sheet (larger sized version here) looks complicated, but should make sense quickly when you review it more closely.

On the left side of the Total Balance Sheet, Assets are divided into two categories: visible and invisible. Visible assets include real assets (like houses) and financial assets (like stocks and bonds). Invisible assets are those relating to human capital.

The raw material of human capital is your age, because all things equal, a low age provides lots of lifespan, which provides time. Time, the “master resource,” offers the opportunity to develop and your deploy human capital to create cash flow and other resources to achieve your goals. Using these cash flows and resources, you can fulfill liabilities on your Total Balance Sheet.

Your human capital is also strongly influenced, of course, by your physical health. You can’t control your health, but you can encourage it through diet, sleep, and exercise.

Emotional health is a key driver for human capital, because when it is strong, energy is higher; when it’s lacking, it is difficult to reliably deploy human capital over time. Family relationships contribute to emotional health, as do one’s stress management, friends, and spiritual life.

Relationships in one’s community through church, civic activity, and clubs help create social capital, which is an accelerant for human capital, allowing it to be developed faster and deployed in more situations. (Translated out of econ-speak, that can mean “it helps you get another job faster.”)

Knowledge (often developed through schooling and professional training) and experience (often obtained through internships, or on the job) round out the drivers of human capital formation.

If your human capital is high and you deploy it effectively with the right mix of industry and serendipity, your future earnings will be high, creating an asset on your Total Balance Sheet that’s very real, even though it may be invisible.

Similarly, on the right side of the Total Balance Sheet, Liabilities are divided into two categories: visible and invisible. Visible liabilities include student loans, credit card debt, mortgage and home equity debt, car loans, and business debt. Invisible liabilities include those relating to community, family, health, and lifestyle aspirations.

Invisible liabilities to the community come in two varieties: voluntary and involuntary.

Voluntary community liabilities might include service on civic boards or a church vestry, or charitable pledges.

Involuntary community liabilities are those relating to future, contingent tax exposure associated with unfunded entitlements and/or deficits run by state, local, and federal government.

(To illustrate this point, is it more congenial to be a high-earning or large-balance-sheet person in a city in California with severely underfunded pension plans, or in Texas, Nevada, or Florida – all high-growth states with no state income taxes?)

Invisible liabilities to family could relate to a spouse, aging parents, or children.

A spouse could have spending problems or a bad marriage could present heightened divorce risks – with all the carnage that usually causes for financial health.

Aging parents could require expensive long term care.

Although children are rewarding in many ways, raising them to adulthood is a seriously large liability, even without the addition of independent primary and secondary school, private college, and graduate school. Adult children can also present ongoing liabilities, such as pressure to subsidize glamorous but non-lucrative careers or help pay for grandchildren’s education.

Health risks and conditions (whether known or unknown) can also present invisible liabilities.

Lifestyle aspirations are one of the largest drivers of invisible liabilities.

A person driven to sustain a higher cost lifestyle will necessarily divert cash flow to fund that lifestyle away from investment in financial capital. They may also work longer hours with higher stress, potentially depleting human capital through reduced health and less time to invest in the relationships that build emotional health and the community activities driving social capital.

The Total Balance Sheet is constantly changing throughout the life cycle, and each person’s is unique.

For instance, a recent engineering school graduate may have high student debt (a visible liability), but also has high future earnings.

A mid-career professional may have retirement accounts providing visible financial assets, valuable job experience, and a wide array of social capital, but lower future earnings and looming, substantial invisible liabilities relating to children’s college costs.

Clients and advisors will make better life cycle estate and financial planning decisions when they take time to reflect on the client’s Total Balance Sheet, how it will change in years ahead, and how various decisions might affect it (for better, or for worse).