Demography, Destiny, and Your Family’s Estate Plan

It’s unclear whether Auguste Comte really said that “demography is destiny,” but you can and should use demographic data to make better estate and financial planning decisions.

It’s unclear whether Auguste Comte really said that “demography is destiny,” but you can and should use demographic data to make better estate and financial planning decisions.

As we’ve noted, an estate plan often represents a set of predictions about a family’s future, predictions that will be improved when the plan considers the family’s Longevity Distribution. Your family has one, it’s unique, and your planning should reflect it.

Demographers and actuaries at the Social Security Administration collect and summarize data on lifespan probabilities. The SSA data assumes a cohort of 100,000 people, and tracks how the cohort will grow smaller over time. By the time male cohort members are about age 80, half of them are projected to be living. For the female cohort, the halfway mark is around age 84. Those male and female halfway marks are the government’s best life expectancy estimates.

I think the distribution of lifespan reflected in the cohorts is much more useful for planning by clients and advisors than a single life expectancy point estimate.

If a financial and estate plan relies on point life expectancy estimates, those estimates are almost certain to be wrong, because half of the cohort members will live less, and half will live longer, than their life expectancy. A robust plan should work well across a wide range of longevity spans for various family members.

I used the SSA cohort data to make sample Longevity Distributions for two different families.

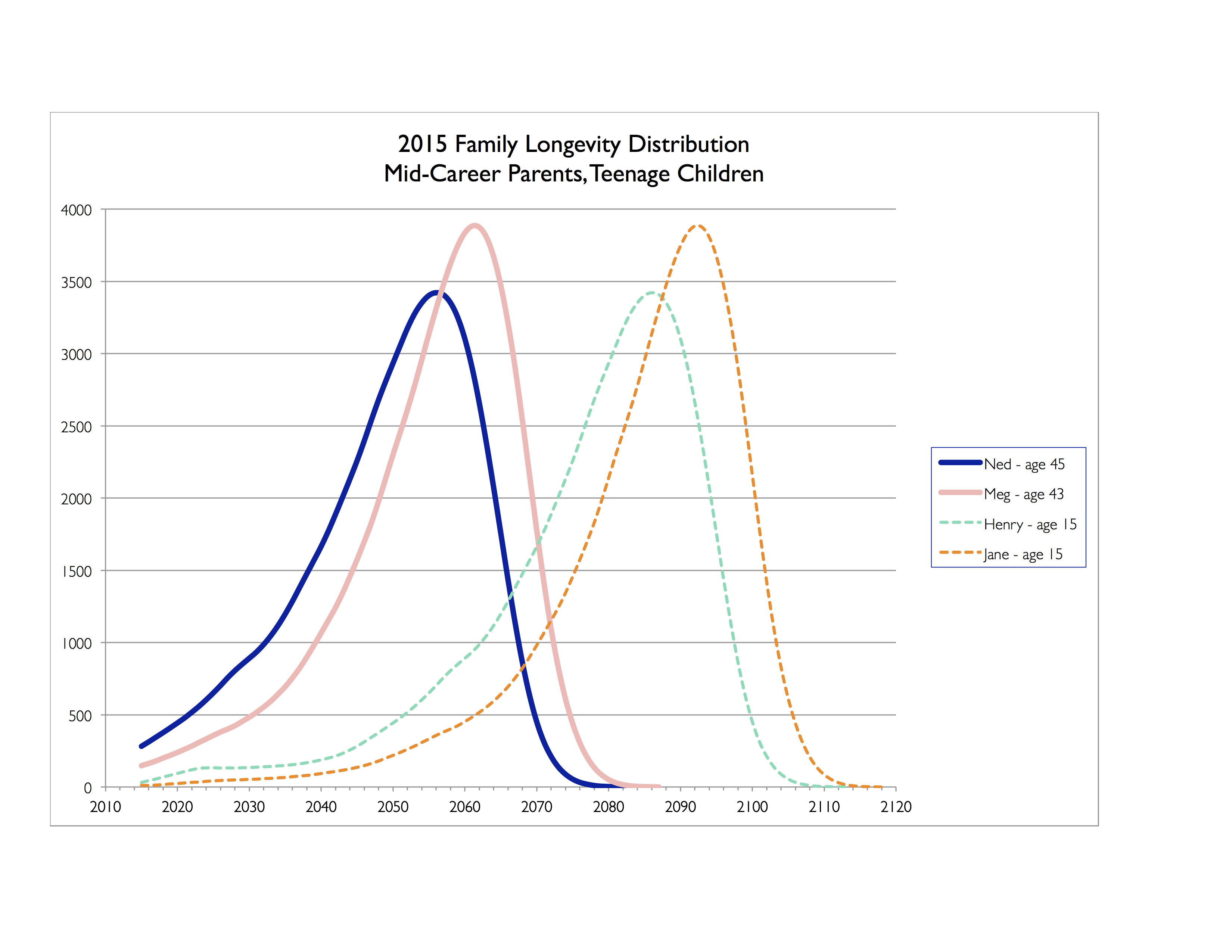

The first distribution is for a family with a mother and father in their mid-40s and son and daughter in their early teens. The curve for father Ned and son Henry shows more dispersion than the curve for mother Meg and daughter Jane. (Women do live longer on average, but their lifespans tend to cluster more tightly.) We can see that this family’s children are likely to inherit from their parents when they’re in their 50s.

The first distribution is for a family with a mother and father in their mid-40s and son and daughter in their early teens. The curve for father Ned and son Henry shows more dispersion than the curve for mother Meg and daughter Jane. (Women do live longer on average, but their lifespans tend to cluster more tightly.) We can see that this family’s children are likely to inherit from their parents when they’re in their 50s.

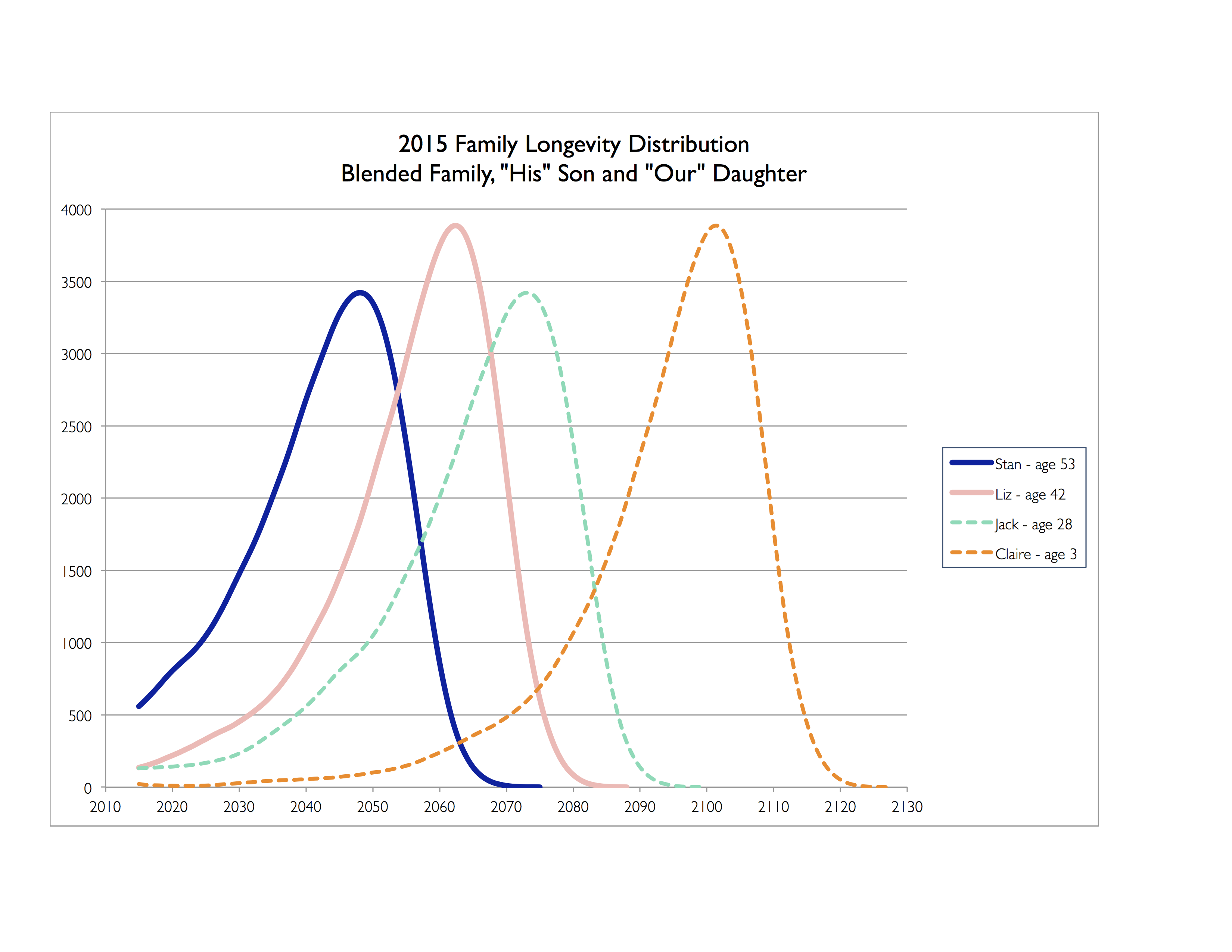

The second distribution is for a blended family with an older father, younger mother, a very young daughter, and a son in his late 20s from the father’s first marriage. Wife Liz is likely to live almost as long as her stepson Jack, and daughter Claire is likely to live an extraordinarily long time.

The second distribution is for a blended family with an older father, younger mother, a very young daughter, and a son in his late 20s from the father’s first marriage. Wife Liz is likely to live almost as long as her stepson Jack, and daughter Claire is likely to live an extraordinarily long time.

Even if the assets and income of these families are similar, isn’t it likely that their estate and financial plans should be designed differently?

Even if Stan and Ned have the same risk tolerance, shouldn’t their financial advisor encourage them to consider different asset allocations?

Wouldn’t the life and long term care insurance needs of these two families be very different?

Yes, those are leading questions – but they illustrate an important point.

While it is true that no one can know what the future holds, a family and its advisors can know, for instance, that 15 years from now, everyone in that family who is still “in the cohort” will be 15 years older. That is knowable, and it has predictable consequences.

The planning environment is unavoidably unpredictable, so when it does present something that is predictable, you should take advantage of it. Plan with the Longevity Distribution in mind.